The Complex Perspective · 2016 Chapter 5 of 12 · ≈ 48 min read

The Economy as a Complex System

What is Economics?

Economics is the science of the economy. It is one of the disciplines with the greatest influence on people’s lives, because economists’ ideas influence politics and, through the media, public opinion. Economists are asked about every economic event: the current economic situation, the investment climate, or the mood on the stock market. Bad economic ideas have already cost many people their lives, for example the nationalization of all means of production under Soviet socialism.

What is economics, or economic science?

To define economics, one must first clarify the concept of an economic good. Goods are products and services. A person’s working time is also a good. Sometimes a good is also called a resource. These goods are usually not available in arbitrary and sufficient quantities. In economics they are therefore called “scarce.” In everyday language, however, “scarce” is used differently. Colloquially, something is scarce when very little of it remains. In economics, “scarce” means that there is not an unlimited amount of it. Oxygen-rich air on the North Sea coast, for example, is not scarce, whereas plots of land near the beach are scarce, meaning available only in limited numbers. Most goods are scarce. A good can be used in different ways: a piece of wood can become a guitar, a piece of furniture, or a pencil. It could also be burned and converted into heat. A violin maker needs different wood than a furniture maker. Who decides which trees should be planted when land is scarce? Wood for violins or for furniture? Who decides how a particular good is used?

Now we are ready for the definition:

Economics is the science of the efficient distribution of scarce goods with different possible uses.

Because human society is a complex system, and because the economy serves to satisfy human needs, the economy is also a complex system. Economics is therefore also the science of a complex system.

Economics has a rather dubious reputation. This is due in large part to the fact that its insights are repeatedly torn out of context and misused for political purposes. One example is Adam Smith’s (1723–1790) “invisible hand.” Smith used this metaphor to describe emergent behavior, because at the time there was no better word for it. People act locally and only for themselves, their families, and their friends, but seen globally, much is guided “bottom-up.” Yet as soon as any economic crisis appears, Adam Smith, and with him the entire market economy, is criticized:

Adam Smith supposedly said that the “invisible hand” would regulate everything at all times. And since the financial crisis is here, the “invisible hand” cannot exist; therefore the market economy is useless and Karl Marx was right after all.

But Adam Smith mentions this “invisible hand” only once in each of his two major works, “The Wealth of Nations” and “The Theory of Moral Sentiments.” The “invisible hand” was therefore never the central point of his work. Nor did he say that it would regulate everything, because Adam Smith belonged to the “constrained vision,” in which human beings, and therefore society, have many flaws, as discussed in Section 3.4.

Economists’ statements are heavily distorted in political debates. Something similar happened to John Maynard Keynes [CK14], who would probably be just as dissatisfied with today’s Keynesianism as Karl Marx would be with Marxism [Des04].

Important: Economists are often misrepresented and misinterpreted.

Criticism of Traditional Economics

Because economics is so important for politics, politically desired but scientifically untenable theories often gain acceptance. This makes further development more difficult. No other science has such old scientists cited so frequently: Adam Smith lived from 1723 to 1790, Karl Marx from 1818 to 1883, and John Maynard Keynes from 1883 to 1946. Economists themselves do not do this, of course, but the general public seems to have “stopped” at an old level of basic economic knowledge.

How did this happen?

Historical Development

Adam Smith’s 1776 book “An Inquiry into the Nature and Causes of the Wealth of Nations” is considered the first modern treatment of economics [Bei07]. It addresses questions such as:

- How is wealth created?

- How is wealth distributed among the population?

- What are the consequences of the division of labor?

- What is productivity?

- Should the state intervene in the economy?

Adam Smith still saw himself as a philosopher, and the book is therefore not mathematical. At that time, mathematics itself was still in its infancy. During Smith’s lifetime, physics had made great progress through Isaac Newton (1642–1726). Newton saw the world through his “mechanical glasses”; for him, the world was one great physical machine. This perspective also influenced philosophy and other sciences [Gil13].

During the “classical period” from 1680 to 1830, the relationship between supply, demand, and price was discovered (see Section 5.3) [Bei07]. The question remained open, however, of how one might name or predict the “correct” price. At the time, people still believed that price was objective rather than subjective. In physics, or Newtonian mechanics, one can use the right formula to make predictions about the future. One can calculate how planets move around the sun or where a pendulum will be in 2 seconds. Economists at the time thought they would gain this predictability if they “mathematized” Smith’s work. With the mathematics then available, that was not immediately possible. Only after calculus had been further developed by Gottfried Wilhelm Leibniz (1646–1716), Leonhard Euler (1707–1783), William Rowan Hamilton (1805–1865), and Joseph-Louis Lagrange (1736–1813), and successfully used for physical and astronomical problems, could economics become more “mathematical” in the period of the marginalists from about 1830 to 1930. This required the work of three economists: Léon Walras, William Stanley Jevons, and Vilfredo Pareto [Bei07].

Mechanics and economics, however, differ greatly. To transfer mathematics to economic problems, several simplifying assumptions had to be made. Léon Walras, for example, took the concept of “equilibrium” from physics. Since then, many economists have occupied themselves with these equilibria. Traditional economics sees the economy through the eyes of physics. Imagine a rubber ball in a very large bowl, moving around inside it. Eventually it comes to rest. Equilibrium is reached. Now someone outside the system has to bump the bowl so that the ball moves again. The economy thus moves from equilibrium to equilibrium. States outside equilibrium are not analyzed. Walras made a trade-off here between the possibility of prediction and the loss of realism. His model can no longer be transferred to the real economy. It is a simplification. For its time, this was of course still a great step. Walras applied mathematics to another field. But his willingness to make simplifying assumptions so that the problem remained mathematically tractable has stayed with economics to this day [Bei07].

William Stanley Jevons (1835–1882) wanted to make human behavior as predictable as gravity. He knew the works of Michael Faraday and James Clerk Maxwell on gravity, magnetism, and electricity as “fields of force.” He assumed that price in economics corresponded to energy in mechanics.

Vilfredo Pareto (1848–1923) was the first to investigate the foundations of game theory (see Section 3.3). Pareto had recognized that most people voluntarily perform only win-win actions. And if everyone wins, general prosperity also increases. He thereby laid the foundation for the assumption that human beings always act “optimally.”

The 20th century then saw the rise of the neoclassical school, in which equilibrium economics was expanded and new variants of simplifying assumptions were tried out. In the 1980s, Paul Romer in particular further developed growth theory, but these theories, too, are all based on “physical mathematics” and differential equations.

Traditional Economics is Based on Physics

Classical physics is deterministic: atoms always behave according to natural laws. If one knows the state of a deterministic physical system, one can make predictions about the future. An atom has no free will, cannot learn from the past, and cannot change its behavior. In order to apply the mathematics developed for physics to economic problems, economists have made many simplifying assumptions over time, including the following [Rid10, Gil13, Kah12, Bei07, Tha15]:

- Complete information: Human beings know all products, all sellers, and all prices.

- Perfect rationality: Human beings automatically do what is optimal, i.e. always make the best move in chess. This model was called “homo oeconomicus.”

- Perfect competition: no monopolies, complete transparency.

- Perfect markets with omniscient participants.

- No transaction costs, such as taxes and fees.

- The assumption that products are sold only on the basis of price, not on the basis of appearance or brand name.

- The assumption that a product costs the same everywhere. In reality, the same product often costs different amounts in different supermarkets.

- All firms work as efficiently as possible and have no “frictional losses.”

- Time jumps from equilibrium to equilibrium.

These assumptions separate economic models from reality. From behavioral economics we know that human beings do not have these capacities (see Section 3.2). Economics has created mechanical models of a complex and dynamic system driven by human beings.

Important: Economists have reduced a complex system to a complicated system.

This is by no means intended to diminish the achievements of economics. Economists have done important work that has a major place in human history. But from today’s perspective of complex systems, traditional equilibrium economics is not correct.

Complex Economics

The Economy as a Network

Leonard E. Read’s story “I, Pencil” offers a beautiful image of the complexity of the world [Rea58]. In this story, a pencil describes its “family tree,” that is, its origin, the materials of which it is made, and who produced those materials. It also describes what, in turn, was necessary to produce those materials. The astonishing statement of this essay is:

No single person can make a pencil alone.

Because doing so requires the products or services of other people. The pencil itself is made of wood, lacquer, and graphite, and at the top it has an eraser held by metal. The wood itself comes from a particular kind of tree that must be neither too hard nor too soft. A pencil must be easy to sharpen; if the wood is too hard, that will not work. The wood comes from a tree felled by a lumberjack with an axe or a chainsaw. Perhaps the wood was transported by truck or rail. The following diagram shows a very small excerpt from the pencil’s “family tree.”

It is the beginning of a truly complex network and a complex system. If one thinks further about it, it almost borders on a miracle that it works. Many different individual parts and subsystems cooperate asynchronously with one another in order to produce a pencil in the end. And all this without central control, without an overall plan. This is what Adam Smith called the “invisible hand” (but only once per book!). Today one might call it “collective intelligence” or a “collective brain.” The knowledge required to make a pencil is widely distributed across society. One of the first economists to examine this more closely was Friedrich August von Hayek (1899–1992) [Hay48]. Hayek was an economist who belonged to the Austrian School of economics. This Austrian School differs from traditional economics because it understands economics as the actions of individuals. The economy is the result of human actions. It is viewed “bottom-up” rather than “top-down.” Mathematical models were therefore rejected. Hayek did not look at the economy through the lens of (physical) mathematics and equilibria. His view was not “distorted” by mathematical models. According to Hayek, the economy is a decentralized system, similar to agent-based modeling. In his 1948 essay “The Use of Knowledge in Society,” one finds a quotation that is remarkable from today’s point of view [Hay48]:

“We must look at the price system as such a mechanism for communicating information if we want to understand its real function—a function which, of course, it fulfils less perfectly as prices grow more rigid.”

That was in 1948: communication and information! These were still completely unfamiliar concepts at the time. In the same year, Claude Shannon published his article “Mathematical Theory of Communication,” which is now considered the foundation of information theory. Friedrich Hayek did not remain unknown either; in 1974 he received the “Nobel Prize” in economics.

Supply, Demand, and Price

Prices communicate information. What information do they contain? How do they do that? And if prices are manipulated, for example through laws, minimum prices, maximum prices, and so on, do they lose this information?

Goods are traded on markets: people can offer goods, and others can buy them. Here one distinguishes between supply (what people want to sell) and demand (what people want to buy). There is a connection, a dependency, among supply, demand, and prices. They are not independent variables, but influence one another. This relationship among supply, demand, and price was discovered earlier, in the “classical period” of economics from 1680 to 1830 [Bei07]. It is also treated in mainstream textbooks, such as Paul Krugman and Robin Wells [KW05]. The following diagram sketches these mutual interactions:

Suppose a test person sees an item in the supermarket that they have used for years and want to continue using because it is so good. The item is on sale and costs only half as much. How many does the test person buy? More than usual, of course, because they stock up, provided the item is not perishable. The lower price leads to more of it being bought. Conversely, purchases are reduced when items become more expensive than before. The test person will try to get the item more cheaply elsewhere or switch to another product. The higher price leads to less of it being bought.

Important: Supply, demand, and prices influence each other and cannot be viewed in isolation.

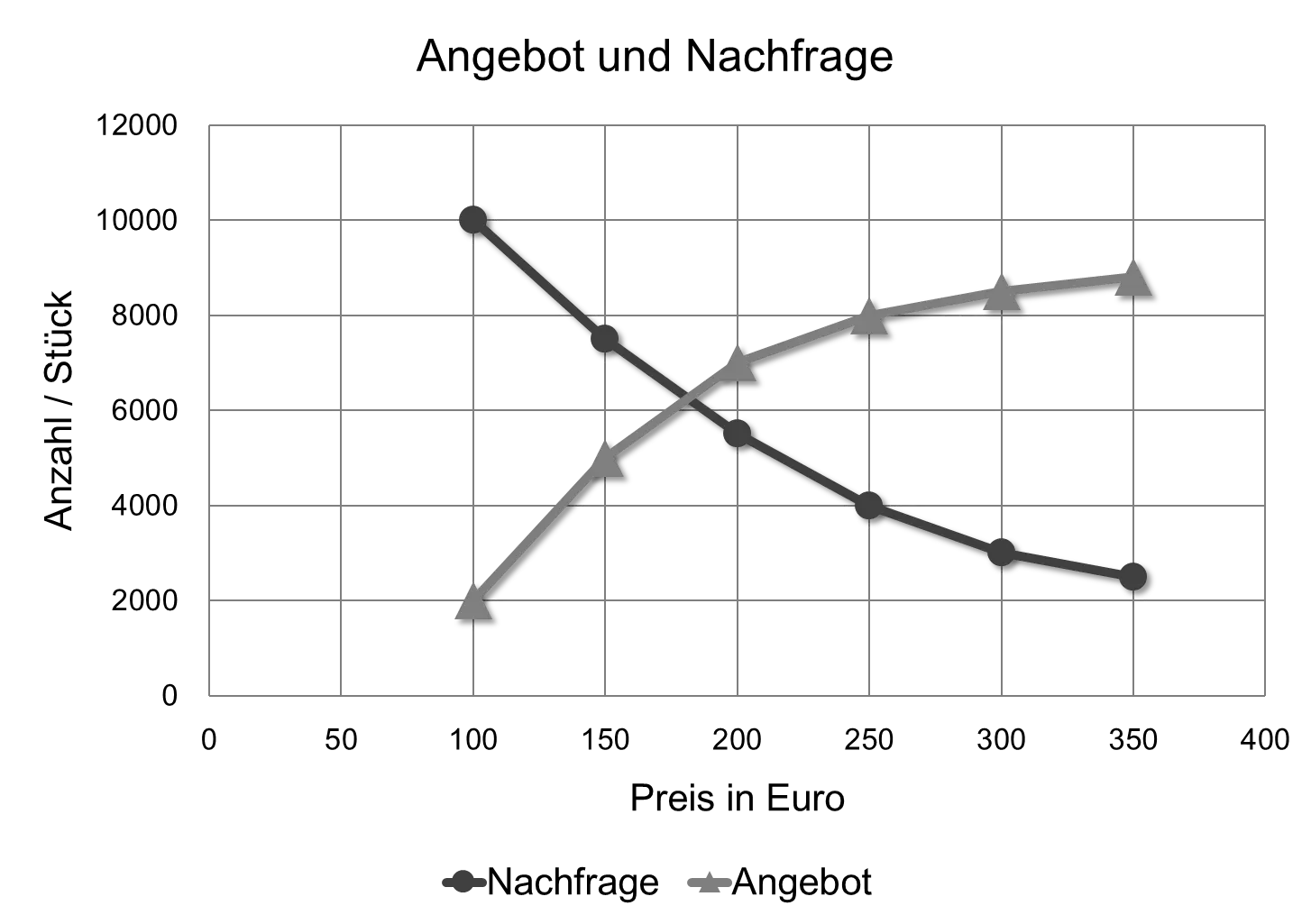

Economists usually explain this relationship in a supply-and-demand diagram:

Two curves are drawn here: supply and demand. The horizontal x-axis shows the price in euros; the vertical y-axis shows the quantity.

The demand curve slopes downward because the more expensive the product becomes, the fewer people want to pay the high price. The supply curve slopes upward because sellers want to sell at the highest possible price. There is a dualism here, two opposing forces that must meet in the middle: sellers generally want to sell something as expensively as possible, while buyers want to buy something as cheaply as possible. Both have to agree on a price. It is an “optimization process,” a “price discovery process,” a kind of auction.

With every purchase, a decision process takes place in a person: “Do I buy this, or do I not buy it?” Millions of times every second on Earth. These are intelligent decisions made in a distributed and decentralized way.

Important: With every purchase or sale, an “optimization” of the economy occurs.

So far, we have considered the relationship only as buyers. Let us put ourselves in the position of a flower seller. We have 1,000 roses and must sell them soon, because they will wilt. We want to work for 8 hours. We set the price at 1 euro per rose, and after four hours we notice that we have already sold 900 roses. We sold them too cheaply! Experienced sellers know this and adjust prices automatically. Large online retailers, for example, measure the sales velocity of every product in units per hour. This lets them calculate when they need to replenish their inventory. If something sells too well, the price is raised; if it sells badly, the price is lowered.

The change in a price over time therefore has a signaling effect and indicates whether supply or demand has risen or fallen. If a good cost 90 euros yesterday and 100 euros today, this may be due to higher demand or tighter supply. In any case, the price change sends the information that something has changed.

Now let us put ourselves in the position of an entrepreneur. Let us assume that the entrepreneur wants to earn as much as possible. But he does not yet know which product he should produce in order to do so. Is it better to produce cleaning products or vacuum cleaners? For the moment, we will ignore the factor of production “knowledge.” Let us assume that an entrepreneur could learn very quickly how to make these things. He will then choose the products on which he can make the most profit, where the “margin” between selling price and production cost is greatest.

To do this, he needs information about past market developments and some idea of what people will buy in the future. An entrepreneur has to guess the future. He conducts an experiment by manufacturing a product. He takes on the “entrepreneurial risk.” Employees take on only a small part of this risk; they receive a monthly salary. A company, however, may have to have a product developed over years and “advance” the investment. The entrepreneur now compares prices and sees that prices for cleaning products have risen sharply. This signals to him that money can be made with cleaning products. He begins producing cleaning products. As a result, there will be more cleaning products next year, and prices will fall again. Contrary to a widespread view, one cannot simply “make” or set prices. Prices arise as an emergent property of a complex system.

What happens to this information when prices are manipulated through political intervention in markets?

- Price ceilings

- Price floors

- Guaranteed purchase prices for green electricity

- Rent caps

- Minimum wages

- Fixed book pricing

According to Paul Krugman and Robin Wells, such interventions have “unpleasant side effects” [KW05]. They even call the chapter “The Market Strikes Back”. The underlying insight is that, in complex systems, an action always has unintended side effects as well. An intervention in the price system therefore produces not only the desired effect, but also side effects that are sometimes difficult to foresee, though often quite logical. If, for example, a state were to set a uniform wage (a maximum and minimum price) so that everyone earned the same, it would not be worthwhile to invest much effort in education. Whether or not one can do mathematics, one would later earn the same.

It is therefore somewhat surprising that politics in Germany is again increasingly introducing price manipulation, for example with the minimum wage or the rent-control brake (Mietpreisbremse). It was a key feature of the “Economic Miracle” (Wirtschaftswunder) that Ludwig Erhard abolished the price controls introduced by the Allies [Erh57].

Important: With the help of the signals sent by price changes, markets allow a certain degree of self-regulation. For this to work, however, the information must still be contained in the prices.

The Economy as an Information System

Information Theory

Prices communicate information, but what exactly is information? The term “information” was precisely defined only in 1948 by Claude Shannon in his article “The Mathematical Theory of Communication” [Gle11]. At that time, however, the main concern was the transmission of messages by radio.

A technician who wants to transmit or store a message needs to know the length of the message, or how much space it needs at minimum on a storage medium. According to the technical definition, the information in a message is therefore the maximally compressed message itself. The length of the message is given in bits. A bit is the smallest distinguishable unit of information, usually represented by 0 and 1. A fair coin toss, in which heads and tails are equally likely, also contains 1 bit of information.

Information can be interpreted as the reduction of uncertainty about the state of the world. Before the coin toss, one is uncertain about the outcome. One has no information about how the coin toss will turn out. Both possibilities are equally likely. The coin toss itself reduces this uncertainty. The same applies to a weather report when one is planning a trip. Before the trip, one is uncertain about the weather at the destination. Will it rain or snow? The information contained in the weather report reduces this uncertainty. Here one must distinguish between absolute and relative information. If one reads the weather report twice, the second reading provides no new information. Relatively speaking, the report no longer contains new information. Absolutely speaking, the same storage space is needed to store the report, so it contains the same absolute information.

Uncertainty about the state of a system is called entropy in physics and information theory. The system must be in exactly one of many possible states. But one does not know exactly which state it is in and can therefore specify only probabilities. Let us once again imagine the “physical” system with the three circles from Section 2.3. From the source code we know where the circles are. We have absolute knowledge. Entropy is minimal. Suppose a computer error had randomly changed all the data. We would not know where the circles are, what size, color, position, and “velocity” they have. We would then have the greatest uncertainty about the system. The circles could be anywhere, and we would know nothing about the state of the system. Entropy would then be maximal.

To reduce entropy in a physical system, one must put in work or energy. To reduce entropy in an information system, one must add information.

Information in the Economy

The entropy of an entrepreneur … oh, a tongue twister … second attempt: the uncertainty of an entrepreneur about the future course of the economy has to be reduced. The entrepreneur wants to produce and sell products. But which ones? And what should they look like? His entropy, or uncertainty, is high. He needs information in order to reduce his entropy, to reduce his ignorance. Just as the physicist takes measurements, the entrepreneur conducts market analyses or tries to generate new information from existing data with the help of data science. Everything serves to reduce ignorance. The same is true for a stock trader. A stock trader does not know how prices will develop, which shares to buy and which to sell. He is uncertain in his assessment of the future. He does not know how a particular company will develop, or how the economy in general will develop. He needs information.

George Gilder worked as a stock trader in the 1970s, and at that time it was important to collect as much information as possible about companies and to find out which companies were doing well and were likely to have a good future [Gil13]. He writes that, as a trader, he had to be constantly looking for surprises, for new information. This allowed him to reduce his uncertainty; he had more knowledge. Stock trading was strongly knowledge-driven.

He also writes that this no longer works today because the information is no longer there. In the 1970s, for example, indices were developed to spread risk. An index is a so-called weighted sum of several values. One example of an index is the average. The average is the sum divided by the number of values. Take, for example, the set of three numbers {1, 3, 8}. The average is (1 + 3 + 8) / 3 = 4. The average is a so-called weighted sum in which the weight is always the same, in this example 1/3: 1/3 * 1 + 1/3 * 3 + 1/3 * 8 = 4. One could now give the middle element more weight, 1/2, and the two other elements less weight, 1/4: 1/4 * 1 + 1/2 * 3 + 1/4 * 8 = 15/4 = 3.75. Such a weighted sum of individual prices, however, destroys the information contained in the individual prices. It “blurs” it.

According to Gilder, indices lead to information dumps and conceal the important information [Gil13]. If one wants to make money on the stock market, one has to be better than the indices. That requires knowledge, information, surprise, deviation from the norm. In stock trading, all known information is already priced in. Only news matters and triggers changes. The trader must evaluate the news and act accordingly, that is, buy, hold, or sell. Originally, indices were developed as a means of reducing risk. The individual indices are robust in Nassim Taleb’s sense (see Section 2.7). But the overall system is not necessarily more robust as a result; it may become fragile. The individual indices cannot crash, but the overall system becomes more brittle [Tal12].

What was once knowledge-driven stock trading has become a game of chance, casino capitalism. According to Gilder, in recent years there have been many additional regulations of the American financial system that aim to avoid risks and crashes, but in reality make information very difficult to find [Gil13].

Important: Today’s stock markets suffer from information loss.

Today’s financial system will be discussed later in Section 11.3.

Markets

Supply and Demand

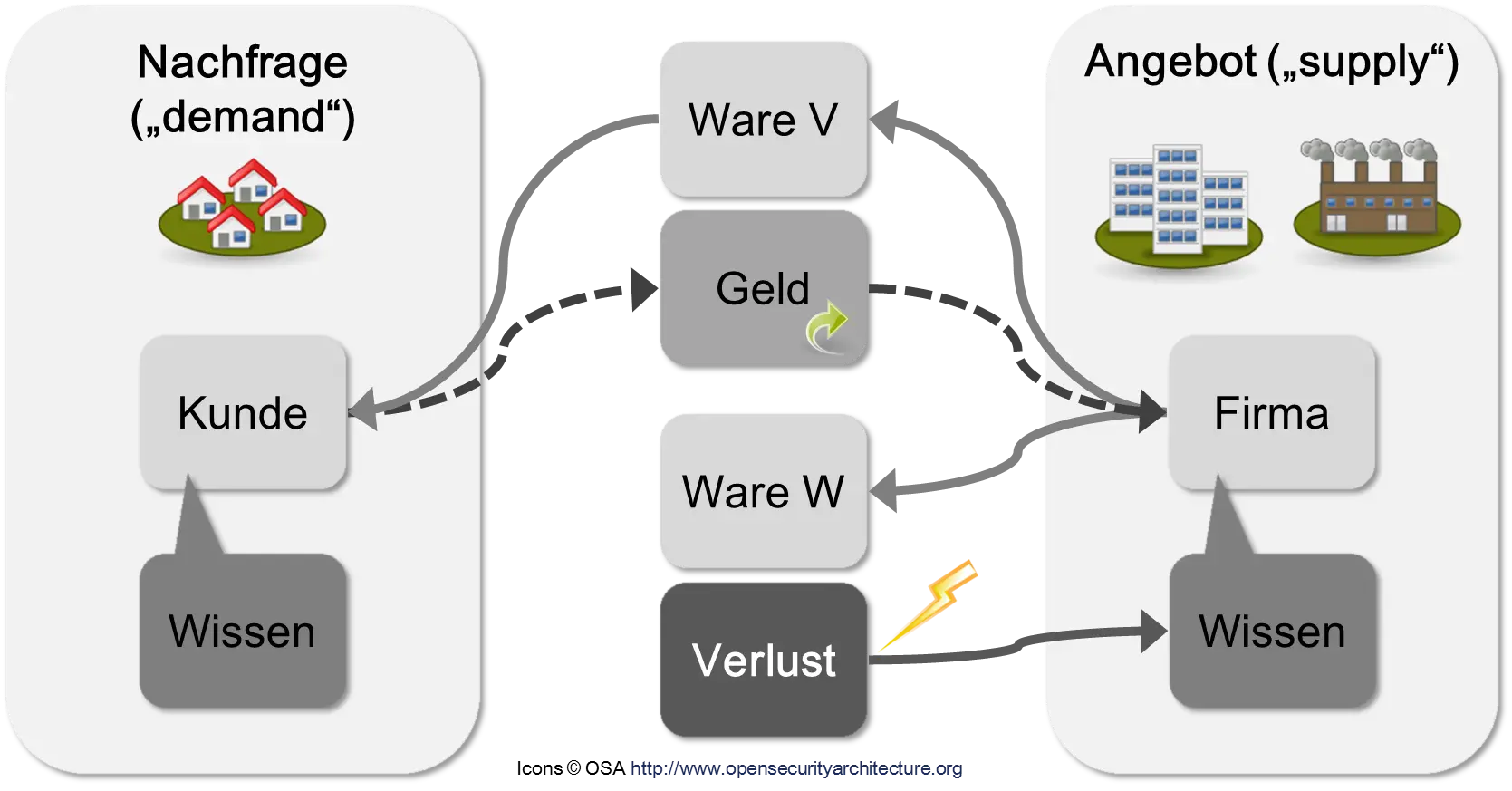

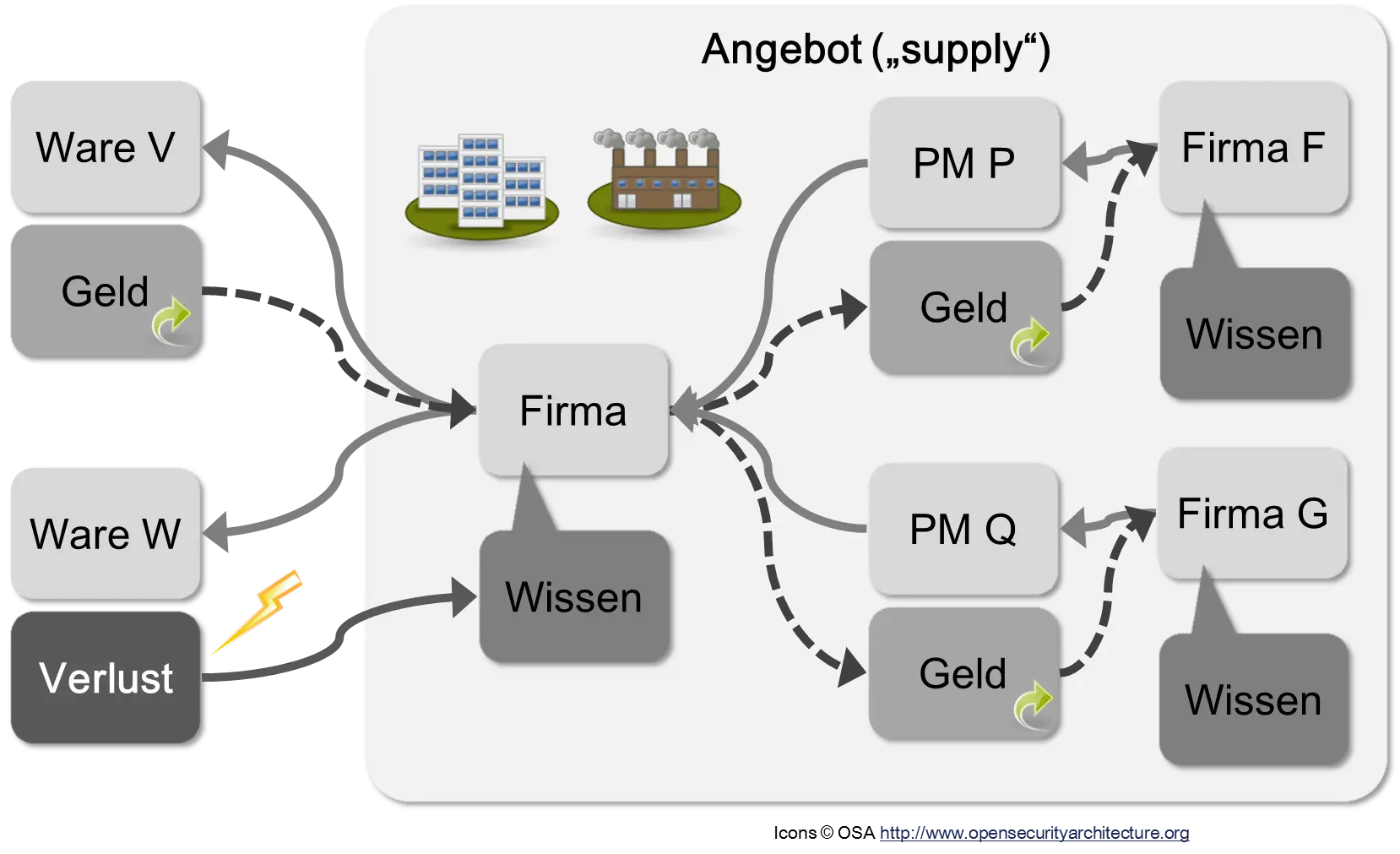

The task of an economy is to provide people with goods and services. The following figure shows a simplified overview.

The economy is divided into two sides: demand and supply. Demand means all customers and buyers of goods and services. Supply comprises all companies. In the figure, one company offers two different goods, V and W. Good V is bought by a customer, who pays for it with money. The customer and the company therefore exchange money for good V. The company gains the information that good V is useful. It also now knows that good W is not needed. The company’s knowledge has increased. One can illustrate a company’s knowledge in a kind of learning curve. For the company, bringing the two goods to market was an experiment, a test. The upper product passed the test; the lower one did not. The company therefore receives both a financial reward and valuable information. For George Gilder, it is an essential element of the market economy that these two kinds of information, the financial reward and the knowledge needed to produce the product, remain together in one organization. The one who earns the money should also be the one who reinvests it. This makes repeated success more likely [Gil13].

In all economic discussions, it is important always to consider both sides: supply and demand. How does a regulation or law affect demand, and what effects does it have on the supply side? Supply and demand stand in a dual relationship to one another. They can be imagined well as the yin and yang symbol of Chinese philosophy.

There is a chicken-and-egg problem here: which came first, the chicken or the egg? Does supply create demand, or does demand create supply? Which side should regulations and interventions in economic policy focus on? Here, too, there are different schools of thought in economics:

- Supply-side policy sees supply as the more important side. Political interventions should support companies and expand supply or make it cheaper.

- Demand-side policy, whose most famous representative was John Maynard Keynes, sees demand as the key element. Interventions here are intended to increase demand.

On which side is there more knowledge? On the supply side or on the demand side?

With the new technical possibilities, socialists came up with the idea that, with the internet and semi-automated factories, a (semi-) socialist planned economy could now be carried out. One would only have to ask customers with an “app” which goods they would like, and then produce accordingly in a “socialist” manner. Demand has been determined, and a large plan is drawn up according to which the supply side is to be organized. In a planned economy, the supply side has no “free will” but must obey the commands of the plan.

Information about customer wishes would indeed be relatively easy to determine, for example with a web page and “apps” for mobile phones. We will set aside here the objection that this would require the “transparent citizen,” without privacy, in which the state would know a person’s entire consumption behavior. So the problems on the demand side are solved. But what about the supply side? Does it simply continue as before? How do new products then arise? In reality, the supply side is much more complicated than the demand side. It is a very complex network, as we know from the story “I, Pencil.” The following figure now also shows two “supplier companies”:

The company uses the means of production (MP) P and Q to produce goods V and W. A means of production is a good used to produce other goods. A robot in a factory is a means of production. So is an oven in a bakery. Whether something counts as a means of production also depends on its use: a laptop used by a journalist to write texts that he sells is a means of production. The laptop is no longer one if the journalist uses it to play computer games. One open question for socialist societies was who decides when something is a means of production and should be nationalized, or when it is private property.

Now company F has used means of production P to produce V. Who decides how long P is used and when it is exchanged for a newer means of production? If it is sold at the right time, perhaps some money can still be made from it. If it breaks, it is repaired or replaced. In an economy where the means of production are privately owned, these decisions are made decentrally; every company decides for itself. Whether the company can produce at all is decided by the customers who buy the product.

The complexity of the supply side of the economy is hidden from many supporters of a “planned” economy. Even if, in the age of the internet, end-consumer demand can be easily determined, who decides which means of production P and Q are manufactured? Which resources should in turn be used to make them?

In many variants of socialism, these means of production are to be nationalized and a centrally planned economy introduced. To create this plan, however, one must possess the knowledge of the supply side. The knowledge distributed among individual firms in a market economy must therefore be centralized. But the “transfer” of knowledge to a planning ministry is anything but simple. Knowledge can only be “learned” by people, not simply “transferred.” This “knowledge problem” of the centrally planned economy comes from Hayek’s work already mentioned [Hay48]. Centralizing the economy would place a great deal of economic power in the hands of a few planning officials. The advantage of a market economy is that both knowledge and power are decentralized; the more distributed, the better [Gil13].

A further question is who determines the price of the means of production if they are all owned by the state. The state would then be seller and buyer in one person. There would be no market for means of production and no prices. Consequently, there can be no economic calculation. When should a means of production be replaced by a new one? Without prices, this cannot be answered efficiently. This argument was published in 1922 by the Austrian economist Ludwig von Mises in his book “Socialism” [Mis49]. The problem, however, affects every monopoly, including large monopolistic companies.

The Market

Supply and demand are brought together in a market. In the physical world, a market is usually a square in the center of a city where merchants once offered their goods. Such marketplaces still exist in many cities, but most consumer goods are traded in supermarkets and department stores.

A market in the theoretical sense is a set of sellers, buyers, goods, and prices. There are several variants:

- A free market is not regulated, i.e. there are no restrictions imposed by the state or others. There are not many of these left in the real world. But much open-source software is still free, such as programming languages and databases.

- In a regulated market, there are state requirements, such as:

- Only certain sellers are admitted, e.g. through licenses, as with taxis or banks.

- Only certain buyers are admitted, as in wholesale trade.

- There are price rules, such as maximum prices or minimum prices.

- There are ecological guidelines.

- Under labor law: a business of a certain size must have a works council.

- In a black market, goods prohibited by the state are sold, such as weapons and drugs. Offers for which the necessary taxes and duties have not been paid also count as part of the black market, for example goods not cleared through customs or undeclared work.

If one wants to write an agent-based model for a simulation, a colloquial description of a market is of course not enough. In their book “Networks, Crowds, and Markets: Reasoning About a Highly Connected World,” David Easley and Jon Kleinberg introduce the mathematical and algorithmic theory of markets [EK10].

Matching Market

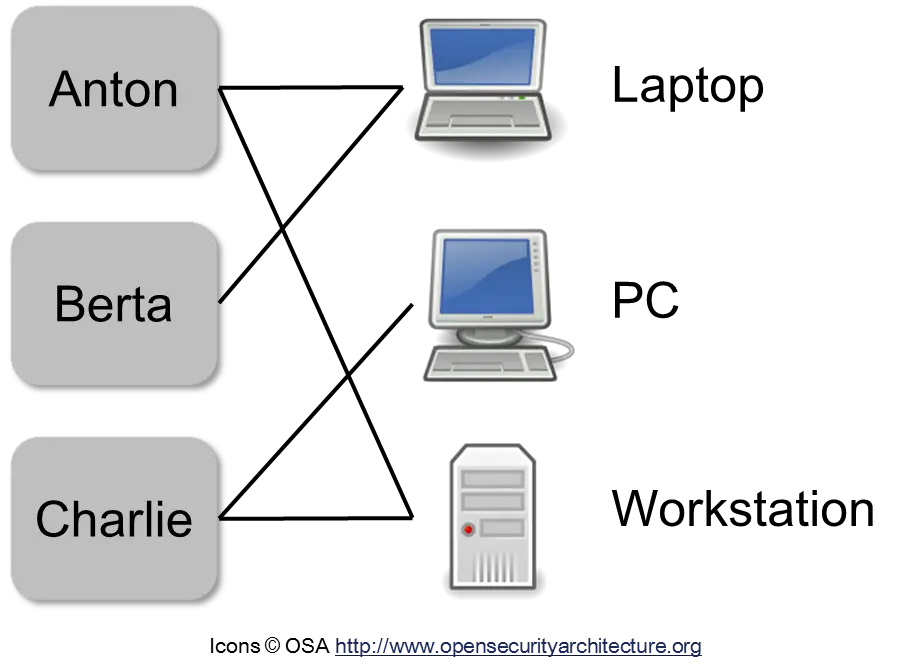

A “matching market” is the simplest possible example of a market. Suppose, for example, that Anton, Berta, and Charlie have founded a startup and have to share a laptop, a PC, and a workstation. But not everyone wants to work on every device. Everyone has preferences. Anton, for example, would work on the laptop and on the workstation, Berta only on the laptop, and Charlie on the PC or the workstation. The following figure shows the three people and the three devices schematically.

The preferences are represented as (undirected) edges between the nodes. Such a graph is called a bipartite graph because it has two different kinds of nodes (people and devices), and an edge always connects the two kinds.

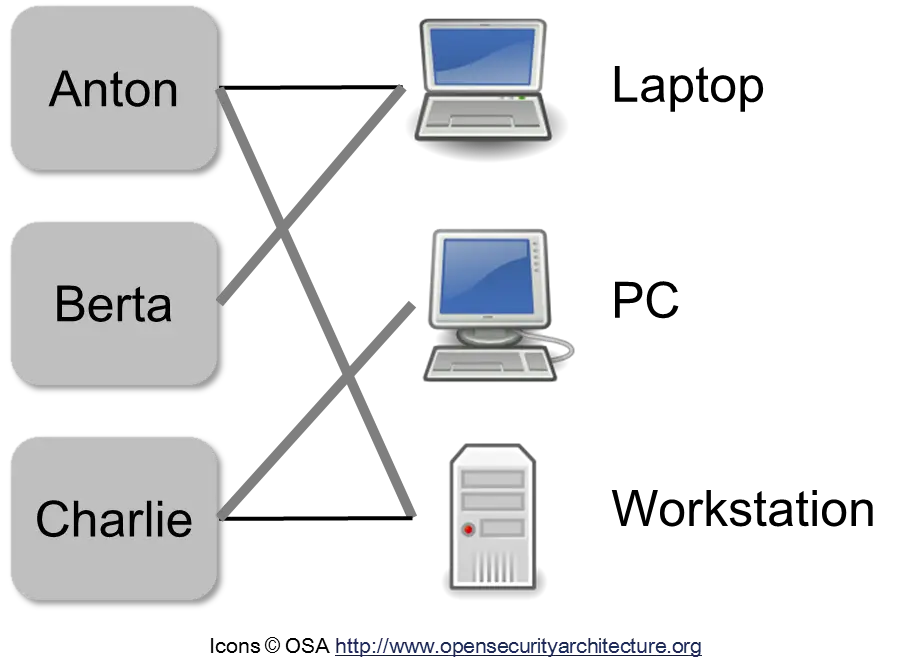

A “matching” is a solution that finds an edge from each person to a different device, that is, finds a device for every person. Many different algorithms have been developed in computer science for this purpose [CLRS09]. In the following figure, such a “matching” is indicated by thicker edges.

Anton takes the workstation, Berta the laptop, and Charlie the PC.

“Matching markets” are the simplest imaginable markets. An algorithm for a simple problem can often be extended. One such extension would be to rank the preferences. Anton could then say, for example, that he would rather work on the laptop than on the workstation. This turns a matching into an optimization problem. One does not want to find just any matching, but the “most optimal” one, so that as many people as possible can work on their favorite device. Algorithms have also been developed for this problem [EK10].

A Market with Prices

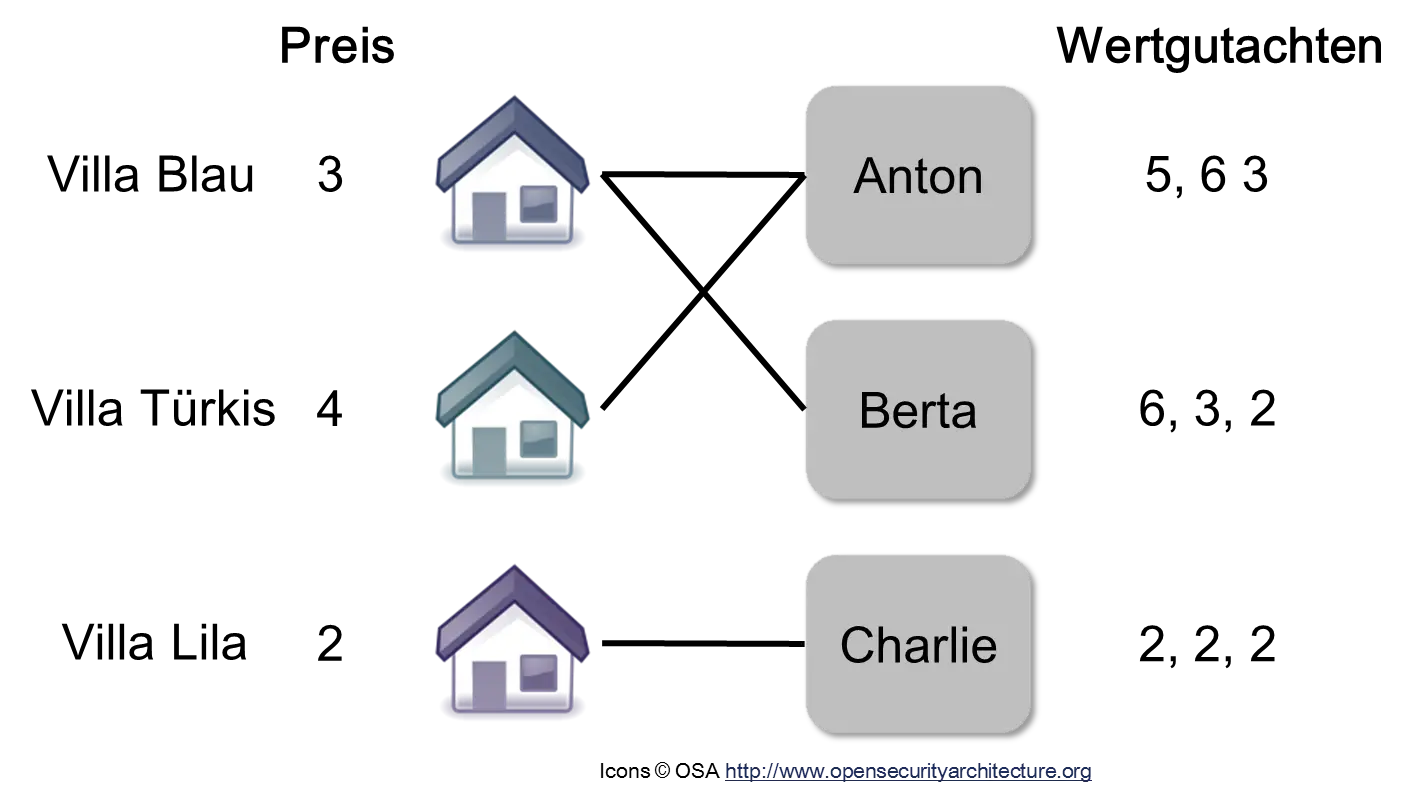

Another extension is prices. For this we use a different example (freely adapted from [EK10]): Anton, Berta, and Charlie were very successful with their startup, and now each wants to buy a villa. There are three villas to choose from: Blue, Turquoise, and Purple. Each villa owner states a selling price: Villa Blue for 3, Villa Turquoise for 4, and Villa Purple for 2.

Anton, Berta, and Charlie each provide a valuation for every house. Anton, for example, estimates the value of Villa Blue at 5, Villa Turquoise at 6, and Villa Purple at 3. For each valuation, the difference from the asking price is then calculated. Anton estimates Villa Blue at 5, while the price is only 3. He therefore makes a “gain” of 5 - 3 = 2. For Villa Turquoise it is also 6 - 4 = 2, while for Villa Purple it is only 3 - 2 = 1. Anton therefore wants to buy Villa Blue or Villa Turquoise, because the difference is greatest there. For this reason, edges have been drawn in the graph above between Anton and these two villas. The same procedure is used for Berta and Charlie.

The new problem is thereby reduced to the known bipartite matching problem from the previous example. In computer science, it is a common technique to reduce new problems to known problems for which a solution method already exists. An optimal solution for a “matching” is called a market equilibrium (“market clearing price”). In this case, Anton buys Villa Turquoise, Berta buys Villa Blue, and Charlie buys Villa Purple.

Important: A market is an algorithm for solving the relationship between supply, demand, and price.

The economics literature contains countless insights about markets; interested readers are referred to the book by Easley and Kleinberg [EK10].

Criticism of the Market Economy

Markets can therefore be formalized and are an algorithm. Some critics speak of “market radicals” or “market radicalism.” This is just as nonsensical as speaking of “mathematics radicals” or “chemistry radicals.”

In political debates, economic crises are often described as “market failure,” usually accompanied by demands for “better” regulation by the state. Critics usually attribute to the market a capability it does not have. A market, for example, can protect the environment only if the environment is also “expensive.” If a company is allowed simply to clear a rainforest for a low price, that is a problem of the forest owner and not of the market. Why does the forest owner sell the wood so cheaply? The owner is probably a state, because a company, being profit-oriented, would sell the forest as expensively as possible. This is an example of the “Tragedy of the Commons.” A market can also be immoral, for example in the brokering of contract killers or dangerous poisons. But that is not a problem of the market itself; it is a problem of the people who offer or buy such things. A market is the result of human actions and therefore also reflects social problems. That is no reason to question the functioning of markets as such.

It should also be emphasized that there are “markets” in which payment is not made with money, but with other social advantages, such as social prestige or sex. The dance floor of a nightclub is also a marketplace.

Profit Orientation, Bureaucracy, and Social Enterprises

Organizations

People organize themselves; they form groups and organizations. They have done this since the time of hunter-gatherers to increase their chances of survival. Later, settlements were added, then cities, empires, and nations. Today, there are also virtual economic and social networks.

In the economy, the most commonly used form of organization is the company. Companies have many advantages over a loose organization of individuals [Mor07]:

- Complex goods can be produced only through cooperation.

- Mass production offers cost advantages; products can be manufactured more cheaply.

- People can cooperate better within a company because communication is more direct and responsibilities and areas of work are clearly defined.

- A company reduces so-called transaction costs. In theory, a company could be run by a single person who purchases all required services from other firms. Because of the many contracts and purchases, this would be cumbersome and would also increase the price of the products.

- Innovations may be worth many millions of euros and are therefore trade secrets. These can be kept secret more easily within a small, close-knit community, such as a startup [TM14].

“Management” has established itself as a technique for administering such organizations. The organization is usually divided into specific parts, personnel are often organized hierarchically, and corporate goals are set. In detail, there are many different possibilities. Gareth Morgan’s book “Images of Organization” offers many perspectives from which organizations can be viewed [Mor07]. In the past, organizations were regarded as machines and consisted of individual departments connected by a centralized bureaucracy. They were highly hierarchical, bureaucratic, and mechanistic. Today, companies are more often seen as organisms connected through a kind of nervous system.

Profit-Oriented vs. Bureaucracy

In the past—put simply and somewhat provocatively—there were only the following two possibilities for the supreme organizational principle of an organization [Mis44]:

- Profit-oriented

- Bureaucratic

A profit-oriented company tries to have more income than expenses. The company can support itself financially and does not need subsidies or tax money. A “profit orientation” permits a simpler organizational structure and “flat hierarchies” [Mis44]. The individual departments of a company can work independently as long as those departments are “profitable.” This allows the owners of the company to say to a department head: “You can do what you want, as long as the numbers are right.” The department head is therefore relatively “free” in what he can do.

An example of this is “franchising.” In “franchising,” licenses are granted for the use of business concepts [GFC13]. The franchisor owns the brand name, design, trademarks, and products, and licenses them to the franchisee. The franchisee is usually an entrepreneur who is financially independent and assumes full financial responsibility. The “franchising” business model also has the advantage that it uses the knowledge about local customers that is available decentrally among the individual entrepreneurs. The service is therefore likely to be better, and the employees know their way around better.

Bureaucracy and bureaucratic methods are very old and are present in the administrative apparatus of every state whose rule extends over a larger territory. “Already the pharaohs of ancient Egypt and the emperors of China built giant bureaucratic machineries,” wrote von Mises [Mis44]. Bureaucracy is the organizational form of the “political means.” What could a king do in earlier times if he wanted to appoint a representative in a distant province? There was a danger that the representative would not be loyal and would “abuse his power.” The king therefore could not tell him, “do what you want,” but had to give him instructions and rules. According to von Mises, state bureaucracy consists in the “appointment” of an official and his obligation to follow certain laws and regulations that he must strictly obey. In bureaucracies, the division of labor is organized through hierarchies and rules. This leads, among other things, to bureaucracies being unable to change by themselves and adapt to new conditions. A bureaucracy is “conservative,” because every official is trained to respect the rules and not question them. A bureaucracy is a complicated system, but not a complex one, because it lacks “bottom-up” processes.

Bureaucracy is the instrument of politics. In a world of ever-faster technological progress, rigid bureaucracy will necessarily always lag behind and be unnecessarily complicated. In Germany, there are regular discussions about the “complexity” of a tax return; people say it should “fit on a beer coaster.” This will never happen, because it cannot be changed either “top-down” or “bottom-up.” Many tax advisers earn their money precisely because of this artificial bureaucratic “complicatedness.”

But bureaucracy also exists in today’s companies. As a rule of thumb, the larger the company, the larger the bureaucracy. Bureaucracy also arises in firms because legal requirements have to be met. These legal requirements cause costs that are passed on to customers through higher prices or to employees through lower wages.

Social Enterprises

Profit orientation does not mean that profit must be “maximized,” that the environment must be damaged, or that employees must be exploited, as is often portrayed in the media. A profit-oriented company actually only needs to earn “enough.” “Fair trade” is one example. In recent decades, companies have emerged that are profit-oriented on the one hand, but pursue specific social goals on the other, such as “fair pay for workers in the so-called Third World.”

The fact that “profit orientation” in today’s companies sometimes takes on such inhuman traits is also due to “capitalism without owners” [Gil13]. Most large companies today are joint-stock companies (Aktiengesellschaften) that belong to no one and where, in the end, no one is truly responsible. The employees of the AG can become wealthy only if they “extract” as much value as possible from the company, as managers do with their high salaries.

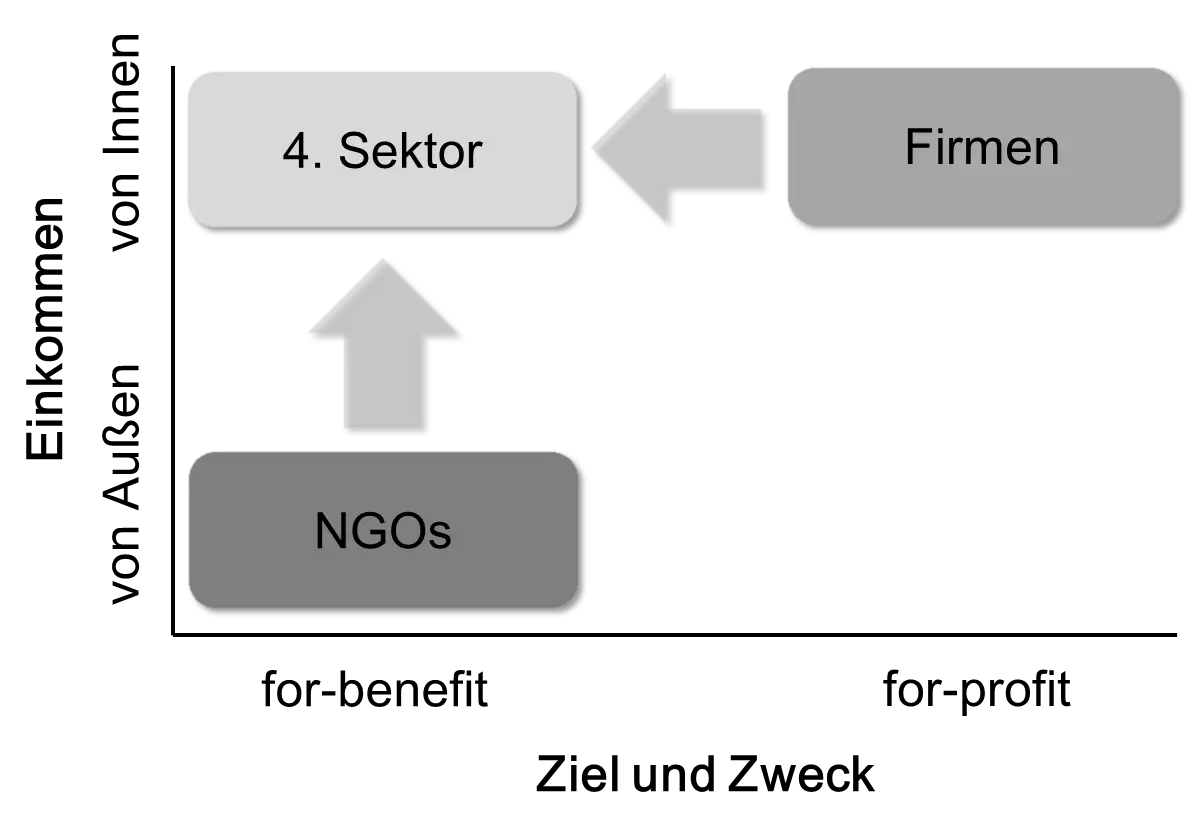

Profit orientation also does not mean that profit has to be monetary profit. An environmental organization can regard its profit as the “protection of endangered species.” A social enterprise can regard its profit as the “number of people with reading and writing skills” or as “what percentage of people can afford a medicine.” In recent years, a new kind of company has emerged here, the “for-benefit” company [CK14], and the so-called “fourth sector.” The following diagram shows the different types of organizations:

Many organizations obtain their income from outside, for example through donations or taxes, such as so-called non-governmental organizations (NGOs). These organizations often have social goals and therefore do not pursue profit maximization. They then most likely have the disadvantage, however, that they are very bureaucratic and the money does not arrive where it is actually supposed to go. Traditional firms, by contrast, are “for-profit” and obtain their income from “inside,” i.e. they generate it themselves, but they have no social goals.

The so-called “fourth sector” (the first sector is the state and is not shown in the diagram) consists of “for-benefit” companies that generate their own income, meaning they are profit-oriented but not profit-maximizing1. They are a mixture of NGO and company that seeks to combine the advantages of both. Such a “for-benefit” company must legally commit itself explicitly to the goals to be achieved. Examples of such goals are “production of a medicine that 95% of the population can afford” or “internet access for 99% of people.”

In many countries, however, the necessary legal framework is still missing to ensure that capital cannot simply be extracted from these firms, thereby converting them into “for-profit” companies. In the United States, experience with this form of company has been gathered since 2010 [CK14]. One task for politics would therefore be to take care of the legal foundations for “for-benefit” companies instead of conducting “political debates” about information technology.

Evolution and Dynamics

The world is constantly changing. Companies develop new products, researchers make new inventions, musicians write new songs, poets write new poems, people change their tastes and habits. The world is dynamic. Heraclitus of Ephesus (520–460 BC) expressed it thousands of years ago: “everything flows” (“panta rhei”). As we will learn in the rest of the book, however, today everything flows faster than before, and in the future it will flow even faster.

People make new technical inventions, which in turn can trigger new social inventions. The telephone, for example, changed people’s social behavior. A factory is an expression of a society’s current state of knowledge about technology, management, psychology, and process organization. Technology influences social and economic life, and vice versa.

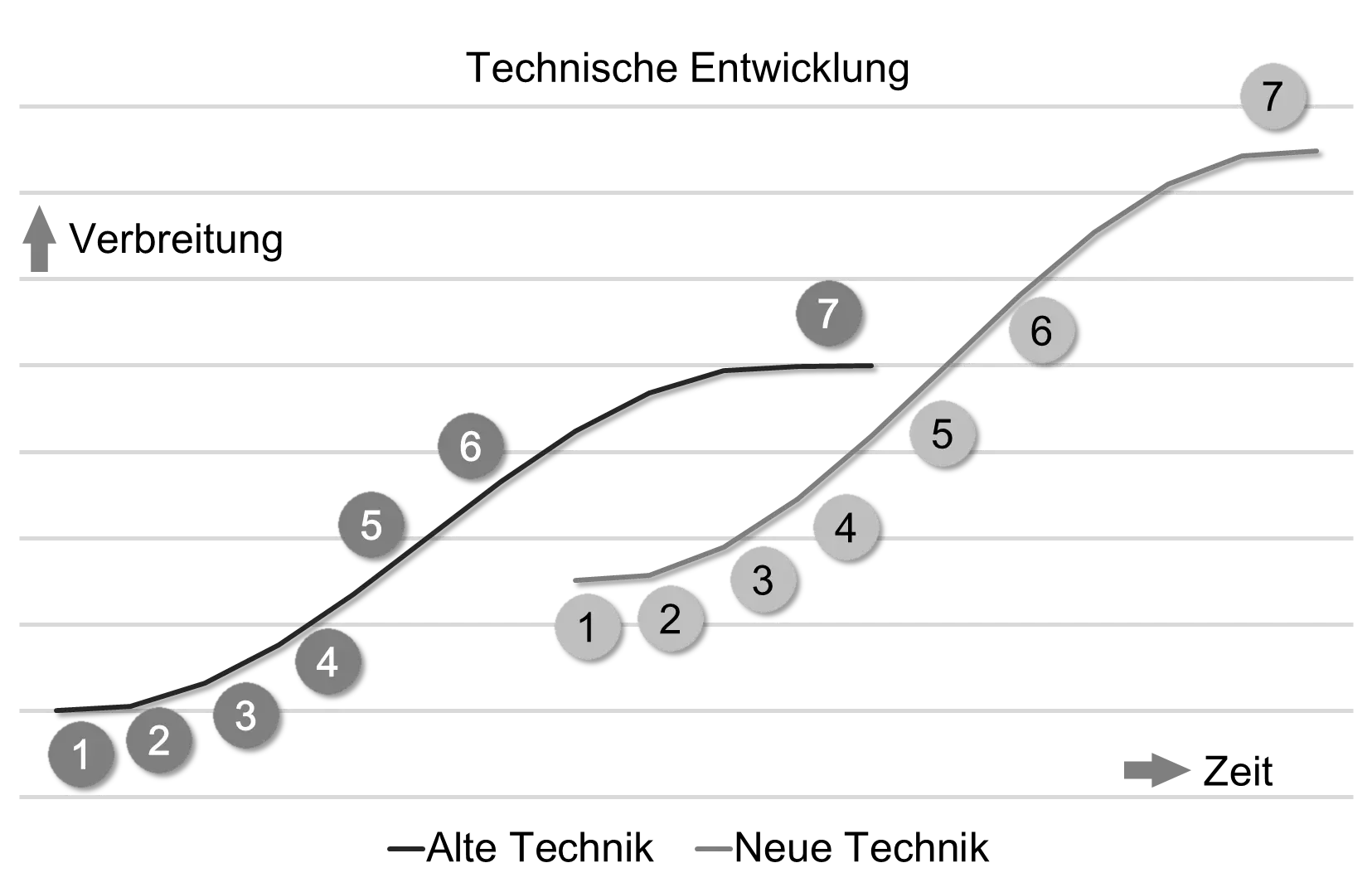

Inventions differ in the influence they have on life in general. Some inventions change life very strongly, such as the internet. And some inventions affect only a small part of humanity, such as a method for producing East Frisian rock sugar (“Kluntje”) more quickly. An invention with very large effects is called a general purpose technology (GPT). Examples include the steam engine, electricity, and information technology (IT). A general-purpose technology is often not very useful on its own, but first needs further complementary inventions that supplement it. People must first find out how best to use such new inventions [BA14]. The introduction of a new invention therefore follows a so-called S-curve, as shown in the following figure:

In the diagram, a new technology replaces an older one. The development has the following phases [Kur06]:

- Dreamers: people dream of the new technology: “Wouldn’t it be nice if …”

- Invention

- Development: the invention must become a product that can be manufactured in mass production.

- Maturation: the technology is gradually improved.

- The technology threatens the old technology, but something is still missing.

- Takeover: the technology takes over the market.

- Antiquity: the technology is obsolete and only something for enthusiasts, such as vinyl records today (approx. 5–10% of its lifespan).

The history of technology is an evolutionary process of successive S-curves. Each phase creates better “tools” for the next phase [Kur06].

It is especially important that society be able to adapt to the new possibilities. If politics, for example, prohibits the use of new robots or makes them more expensive, development is delayed [BA14]. Today, many companies from the so-called sharing economy, such as Uber or Airbnb, are highly controversial. Many established companies demand political action against the new competition.

When something completely new is discovered in a science, such as the theory of relativity in physics, one speaks of a “paradigm shift,” which also follows such an S-curve [Kuh12]. In a paradigm shift, a large part of previous knowledge is replaced because it no longer fits the new paradigm. During a paradigm shift, the sciences also see heated debates between established scientists of the old paradigm and the “innovative” ones. Because science takes place mainly in state universities and research institutions, and is organized bureaucratically and hierarchically, the “newcomers” have a much harder time here than in a market economy. In a market economy, they can do their own “thing” and found a startup, while in the university system one advances only if this has been approved by hierarchical superiors.

Innovations through Collective Intelligence

There are various theories about how innovations arise. The most plausible is the theory of combinatorial innovation [BA14]. According to this theory, innovations arise through new combinations of already known parts. This “combination” is usually not trivial, and finding it can require a great deal of work.

An “inventor” today is usually no longer a single person working alone in a “quiet” room, but a group of specialists who share their knowledge. In an invention, known parts must be connected in new ways: a database, a web server, an app for mobile phones, and so on. The internet is used to exchange ideas. If a technical term is unknown, it is googled. If the database returns a strange error message, one checks the manufacturer’s service portal or an open-source portal.

The more of these “inventors” have internet access, the more inventions can be made. The more inventions have been made, the more building blocks there are for further inventions. Here growth accelerates. Humanity is a networked problem-solving process. A “collective intelligence” has emerged [Hin13, BA14].

Complex Economics

Once one is familiar with complex systems and agent-based modeling, economics no longer seems to be at the current state of the art. Many mathematical-economic analyses use equilibria derived from physics. If one looks at a typical introduction to economics, such as the one by Paul Krugman and Robin Wells [KW05], one is initially surprised that the economy is treated only from a bird’s-eye view and is more a statistical science than a causal one.

But this will probably not remain the case for much longer, because economics is at the beginning of a paradigm shift: through the theory of complex systems and agent-based modeling, economics in the 21st century is supposed to become a “real” science, complexity economics [Bei07, Art14, CK14].

According to Eric D. Beinhocker, this “paradigm shift” should take place as quickly as possible, because it has major consequences [Bei07]. Many previous insights in economics, politics, and society are at best approximately correct, and many parts are wrong. Politics therefore tends to cause damage rather than make useful decisions. According to Beinhocker, new economic theories have always triggered major changes in practice: Adam Smith, for example, led to free trade and the Industrial Revolution. Karl Marx led, on the one hand, to revolutions and the socialism of the Soviet Union (Marxism-Leninism), and on the other hand to the welfare state and social democracy. The German party SPD, for example, named “democratic socialism” as its goal in its 2007 “Hamburg Program” and described “Marxist social analysis” as one of its roots [SPD07]. The neoclassical theories of the last half of the 20th century led to today’s globalized “casino capitalism” [Bei07].

The following table summarizes the differences between complex and traditional economics:

| Complex Economics | Traditional Economics | |

|---|---|---|

| Dynamics | Open, dynamic, non-linear | Closed, linear, equilibrium |

| Agents | Individuals, incomplete information, make mistakes, adaptive, learn | Collective, perfect rationality, complete information |

| Networks | Explicitly defined | Implicit, e.g., auctions |

| Emergence | Yes | Micro- and macroeconomics are different subjects, emergence is interdisciplinary |

| Evolution | Possible through differentiation, selection, and reinforcement | No changes |

Economics therefore also faces major changes. Because of the “Twin Peaks” problem already mentioned, however, these changes will probably take place rather slowly. But they will take place. The theory of complex systems and the “bottom-up” perspective of agent-based modeling allow a better view of reality than the differential equations used so far.

-

See also http://www.fourthsector.net/. ↩